What is Account Reconciliation?

Account reconciliation is a critical accounting process that compares two sets of financial records to ensure accuracy and consistency. It confirms that the recorded amounts leaving an account match the actual amounts spent, ensuring that the general ledger (GL) is correct. This process helps detect discrepancies such as errors, omissions, or fraudulent activities, which can then be investigated and corrected.

Why is Account Reconciliation Important?

Account reconciliation is essential for maintaining the integrity of financial records. It helps:

- Prevent errors on the balance sheet.

- Detect and prevent fraud.

- Ensure compliance with regulatory requirements.

- Provide accurate financial statements, which are vital for decision-making by internal and external stakeholders.

- Facilitate audit processes by maintaining detailed and accurate financial records.

What are the Benefits of Account Reconciliation?

The key benefits of account reconciliation are:

- Improved Accuracy: Ensures that financial statements are accurate by identifying and correcting discrepancies.

- Fraud Detection: Helps uncover fraudulent activities by highlighting unexplained variances.

- Regulatory Compliance: Ensures that the company meets regulatory and audit requirements.

- Financial Health: Provides a clear and accurate picture of a company’s financial health, aiding in better decision-making.

- Efficiency: Regular reconciliation can streamline accounting processes and reduce the time spent on audits.

What are the Challenges of Account Reconciliation?

Account reconciliations come with their own set of challenges. Here are some of the most common hurdles you might encounter during the reconciliation process.

- Manual Processes: Manual reconciliation is time-consuming and prone to errors.

- Data Volume: High transaction volumes can make reconciliation complex and labor-intensive.

- Discrepancies: Identifying and resolving discrepancies requires thorough investigation and can be challenging.

- Resource Intensive: Requires significant time and effort from accounting staff, particularly during peak periods such as month-end.

What are the Types of Account Reconciliation?

Here are the various types of account reconciliation you should be aware of, each serving a specific purpose in maintaining accurate financial records.

- Bank Reconciliation: Compares a company’s internal records with bank statements to ensure they match.

- Accounts Receivable Reconciliation: Ensures that amounts owed by customers match the recorded receivables.

- Accounts Payable Reconciliation: Ensures that amounts owed to suppliers match the recorded payables.

- Inventory Reconciliation: Matches physical inventory counts with accounting records.

- Payroll Reconciliation: Verifies that payroll records match bank statements and tax filings.

- Credit Card Reconciliation: Compares credit card statements with internal records to ensure accuracy.

- Fixed Asset Reconciliation: Ensures that recorded fixed assets match the physical assets.

- Expense Reconciliation: Matches expense reports and receipts with accounting records.

How Does Account Reconciliation Work?

The account reconciliation process involves several steps to ensure accuracy and consistency in financial records. Here's a detailed breakdown of each step:

- Collect Financial Records: Gather bank statements, invoices, receipts, and other relevant documents.

- Identify Discrepancies: Compare internal records with external documents to identify any differences.

- Investigate Discrepancies: Determine the cause of discrepancies by reviewing contracts, contacting vendors, or checking for accounting errors.

- Make Adjustments: Correct errors in the accounting system by adjusting entries or updating records.

- Document Changes: Maintain records of all adjustments for future reference and audit purposes.

- Verify Accuracy: Double-check the reconciled accounts to ensure all discrepancies have been resolved.

- Repeat Regularly: Perform reconciliation regularly (e.g., monthly) to maintain accurate financial records.

What are the Best Practices for Account Reconciliation?

Implementing best practices for account reconciliation can greatly improve accuracy and efficiency. Here are some key practices to consider:

- Automate the Process: Use software tools to automate reconciliation tasks, reducing errors and saving time.

- Standardize Procedures: Implement standardized procedures for reconciliation to ensure consistency.

- Regular Reviews: Conduct regular reviews and reconciliations to maintain accuracy.

- Segregate Duties: Separate duties among staff to prevent fraud and errors.

- Training: Ensure that staff are well-trained in reconciliation processes and tools.

- Use Technology: Leverage advanced tools and technologies such as AI and machine learning to enhance reconciliation efficiency and accuracy.

How Solvexia Helps with Account Reconciliation

Solvexia offers robust solutions to streamline and automate account reconciliation processes, ensuring accuracy and efficiency. With Solvexia, businesses can:

- Automate data collection and reconciliation tasks.

- Identify and resolve discrepancies quickly.

- Maintain accurate and up-to-date financial records.

- Ensure compliance with regulatory requirements.

- Improve overall financial management and reporting.

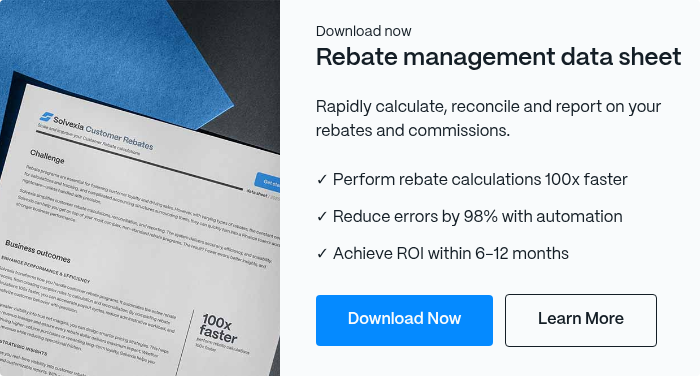

Using Solvexia, leading companies run their reconciliations 100x faster and with 98% fewer errors.