Reconcile Bank Statements with Automation

In today’s fast-paced financial environment, automating the bank statement reconciliation process is becoming essential for businesses seeking efficiency and accuracy.

Automation streamlines the reconciliation of bank statements by minimizing manual data entry, reducing errors, and speeding up the process, thus empowering companies to maintain precise financial records effortlessly.

In this article, we will how to reconcile bank statements, along with how automation software can be of great service to businesses of any size.

Coming Up

What is Reconciling Bank Statements?

Reconciling bank statements is the process of comparing a company's financial records with its bank statements to ensure accuracy and consistency. It involves checking that all transactions listed in the bank reconciliation statements match those recorded in the company’s accounting books.

This process helps identify discrepancies, such as missing transactions or errors, and ensures that the financial records accurately reflect the company's cash position.

Regularly maintaining the transaction reconciliation process helps prevent fraud, detect errors, and maintain accurate financial reporting. It’s a key part of effective financial management and internal control. Also important is the bank reconciliation statement format. This can make a huge difference when it comes to precision, decision-making and compliance.

What are the Benefits of Reconciling Bank Statements?

There are many benefits in reconciling bank statements. Let’s take a closer look at some of the most important.

1. Accuracy in Financial Records

Bank reconciliation statements ensure that a company’s financial records are errorless and up-to-date. Compare the company's ledger with the bank’s records.

Look for discrepancies such as errors in recording transactions, missed entries, or duplicate entries to identify and correct them. This process helps maintain reliable financial data, which is crucial for making informed business decisions and preparing precise financial statements.

2. Fraud Detection

The transaction reconciliation process helps in detecting fraudulent activities early. By scrutinizing transactions and comparing them against bank records, businesses can spot unauthorized transactions or irregularities that might indicate fraud.

This proactive approach helps in mitigating the risk of financial loss and strengthens internal controls.

3. Cash Flow Management

Meticulous reconciliation provides a clear picture of the company’s cash flow. It helps in identifying timing differences between when transactions are recorded and when they actually clear the bank.

Understanding these discrepancies aids in better cash flow planning and management, ensuring that the business can meet its financial obligations and optimize its cash reserves.

4. Compliance and Reporting

For many businesses, reconciling bank statements is a regulatory requirement. Regular reconciliation ensures compliance with accounting standards and financial regulations.

It also provides a solid foundation for preparing financial reports and statements, which are essential for audits and tax filings.

5. Improved Financial Management

Consistently following bank reconciliation process steps can enhance overall financial management by providing insights into transaction patterns and account activities.

This information can be used to refine budgeting, improve financial strategies, and make more informed financial decisions.

With automation software that executes bank statement reconciliation, companies can remove key person dependencies, connect and process all data seamlessly, access audit trails, save time, and reduce errors. All the benefits of completing consistent bank statement reconciliations can be realized without a second thought.

What are the Steps to Reconcile Bank Statements?

Now, let’s walk through the steps required to reconcile bank statements. Each one of these bank reconciliation process steps is vital to avoid errors and ensure compliance.

1. Gather Documents

Start by collecting the necessary documents: the bank reconciliation statement and the company's cash book or accounting ledger. Ensure you have the most recent bank statement, which can typically be accessed online or through bank correspondence.

Collecting documents manually is one of the most time-consuming aspects of bank reconciliation. With automation software, you can alleviate this burden and automatically centralize all necessary data.

2. Compare Transactions

Begin the transaction reconciliation process by matching each transaction on the bank statement with those recorded in the company’s ledger. Check off each transaction in both documents to ensure that they align. Look for deposits, withdrawals, and other transactions to verify they match across sources..

3. Identify Discrepancies

During the transaction reconciliation process, you may encounter inconsistency while comparing transactions such as missing entries, errors, or unrecorded bank fees. Note these differences for further investigation.

Common issues include checks that haven't cleared yet or errors in recording amounts- these are explainable, and therefore, do not warrant a reason to worry.

4. Adjust Records

Make adjustments in the company’s cash book for any disparities identified. This could involve adding missed transactions, correcting errors, or noting bank fees that weren’t previously recorded. Ensure that all adjustments are accurately reflected in the ledger. This is an important part of the transaction reconciliation process.

5. Recalculate Balances

After adjusting the records, recalculate the ending balance in the company’s ledger. Compare this adjusted balance with the ending balance on the bank statement. They should match, or be reconciled with noted differences like outstanding checks or deposits in transit.

6. Document the Reconciliation

Once the balances match, document the transaction reconciliation process. Record any adjustments made and ensure that the bank reconciliation statement is reviewed and approved if necessary. This documentation serves as a record for future reference and audits.

7. Review and File

Finally, review the reconciled bank statement and ledger to ensure everything is correct. File the documents and reconciliation report in an organized manner for future reference and to comply with accounting policies. Regularly repeating this process will help maintain correct financial records.

How Often Should You Reconcile Bank Statements?

Bank statements should generally be reconciled on at least a monthly basis. This frequency aligns with the typical bank reconciliation statement cycle and ensures that any discrepancies, errors, or fraudulent transactions are identified and addressed promptly.

This monthly process helps you identify any inconsistencies, such as unauthorized transactions or errors, while also giving you a clearer picture of your cash flow. For businesses, more frequent reconciliations – weekly or bi-weekly – are often recommended to maintain tight control over finances and catch any issues early.

Additionally, if you have high transaction volumes or fluctuating cash balances, more frequent checks can help you stay organized and prevent financial mismanagement. This is particularly important if you use multiple payment providers such as Amazon, ebay, Stripe,Worldpay etc.

Monthly bank reconciliation statements help maintain accurate financial records, support effective cash flow management, and ensure compliance with accounting standards.

For businesses with high transaction volumes or complex financial activities, more frequent reconciliations – such as weekly – might be beneficial to catch issues early and maintain tighter financial control.

Since manual account reconciliation is time-consuming and error-prone, you can rely on automation software to streamline the reconciliation process with utmost confidence in its precision.

What are the Challenges During Bank Reconciliation?

Bank reconciliation can present several challenges that can complicate the process:

1. Identifying Discrepancies

One common challenge is identifying discrepancies between the bank reconciliation statement and the company’s records.

Errors may arise from missed entries, incorrect amounts, or timing differences such as outstanding checks or deposits in transit. These discrepancies can make it difficult to reconcile balances accurately.

2. Timing Issues

Timing differences are another challenge. Transactions may appear on the bank reconciliation statement at different times than when they are recorded in the company's ledger.

For example, checks issued by the company might not have cleared the bank yet, creating a temporary mismatch that requires careful tracking.

3. Error Correction

Correcting errors in either the bank reconciliation statement or the company’s records can be complex. Mistakes might include data entry errors or bank fees not previously recorded.

Ensuring that all corrections are accurately reflected in the financial records requires meticulous attention to detail.

4. Fraud Detection

Spotting fraudulent activities or unauthorized transactions during the bank reconciliation process can be challenging. However, these mismatched records might not always indicate errors; they could be signs of fraudulent activities, necessitating thorough investigation and heightened vigilance.

5. Documentation and Compliance

Maintaining thorough documentation and adhering to compliance standards adds another layer of complexity. Properly recording adjustments and ensuring that all bank reconciliation process steps are well-documented is essential for audit trails and regulatory compliance.

Bank reconciliation software includes this function automatically, so your team can always have access to version history and maintain internal control. In fact, bank reconciliation software prevents every pain point listed above by automating the entire process and reducing the time-consuming aspect of transaction matching and having to perform lengthy investigations.

What are Best Practices for Bank Reconciliation?

Bank reconciliation is a critical financial process that ensures precision between a company’s accounting records and its bank statements.

Proper bank reconciliation helps in maintaining precise financial records, detecting errors or fraud, and ensuring overall financial health. Here are some best practice tips to streamline and enhance the bank reconciliation process.

1. Use Automation

First and foremost, leveraging an automation solution will streamline your reconciliation processes, along with other critical finance functions. By connecting data, your team can collaborate easily, access the information they need, and meet month-end close deadlines without worry.

2. Establish a Routine Schedule

Reconcile bank statements monthly or more frequently if needed. Regular reconciliations help catch discrepancies early and maintain accurate records. With automation software, even daily reconciliation is possible!

3. Use Reliable Accounting Software

Opt for accounting software that integrates with your bank accounts and automates reconciliation tasks. This reduces manual effort and minimizes errors.

4. Maintain Accurate Records

Record transactions promptly in your ledger and ensure that all entries match your bank statement. Timely and accurate record-keeping prevents discrepancies.

5. Verify Transaction Details

Carefully match each transaction on the bank reconciliation statement with those in your records. Check amounts, dates, and descriptions to ensure consistency.

6. Address Discrepancies Promptly

Investigate and correct any discrepancies found between the bank reconciliation statement and your ledger. Adjust your records to reflect the latest, correct information.

7. Implement Internal Controls

Separate duties among employees to prevent errors and fraud. Regularly review bank reconciliation process steps and perform internal audits for additional oversight.

8. Document the Process

Keep detailed records of each reconciliation, including adjustments and findings. Documentation supports careful financial reporting and provides an audit trail.

By following these best practices, businesses can ensure a smoother and more clear-cut bank reconciliation process, enhancing overall financial management.

How Can Automation Help Reconciling Bank Statements?

Automation significantly enhances the bank reconciliation statement process by streamlining tasks and reducing manual effort. Automated bank reconciliation process tools can directly import bank statements into accounting software, minimizing the need for manual data entry and reducing the risk of errors.

These tools automatically match transactions between the bank statement and the company’s ledger, highlighting discrepancies and saving time spent on manual checks.

Automated systems often feature algorithms that identify and categorize transactions, making it easier to spot inconsistencies such as duplicate entries or missing transactions. They also provide real-time updates and alerts for any discrepancies or unusual activities, enabling quicker resolution.

Additionally, automation ensures consistency and accuracy by applying predefined rules and reducing human error. It helps maintain a clear audit trail by documenting each reconciliation step, which is crucial for compliance and review purposes.

Overall, automation in bank statement reconciliation speeds up the process, enhances accuracy, and allows financial professionals to focus on more strategic tasks rather than tedious manual reconciliation.

The Bottom Line

Reconcile bank statements with automation to transform a traditionally manual and error-prone process into a streamlined, accurate, and efficient task.

By leveraging automated tools, businesses can achieve real-time accuracy, reduce manual workload, and enhance financial oversight, ultimately leading to better financial management and strategic decision-making.

FAQ

Intelligent reconciliation solution

Intelligent rebate management solution

Intelligent financial automation solution

Intelligent Financial Automation Solution

Intelligent financial automation solution

Intelligent financial automation solution

Intelligent financial automation solution

Intelligent financial automation solution

Intelligent regulatory reporting solution

Free up time and reduce errors

Recommended for you

Request a Demo

Book a 30-minute call to see how our intelligent software can give you more insights and control over your data and reporting.

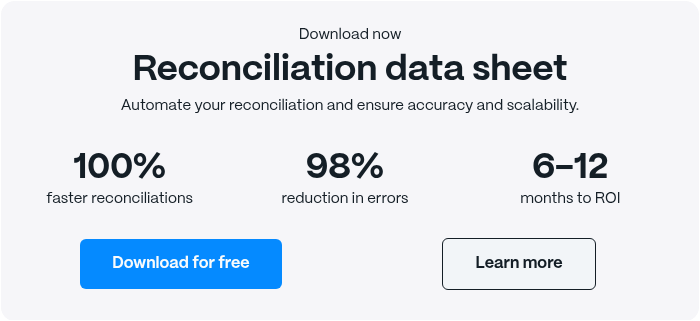

Reconciliation Data Sheet

Download our data sheet to learn how to automate your reconciliations for increased accuracy, speed and control.

Regulatory Reporting Data Sheet

Download our data sheet to learn how you can prepare, validate and submit regulatory returns 10x faster with automation.

Financial Automation Data Sheet

Download our data sheet to learn how you can run your processes up to 100x faster and with 98% fewer errors.

Financial Automation Data Sheet

Download our data sheet to learn how you can run your processes up to 100x faster and with 98% fewer errors.

Financial Automation Data Sheet

Download our data sheet to learn how you can run your processes up to 100x faster and with 98% fewer errors.

Financial Automation Data Sheet

Download our data sheet to learn how you can run your processes up to 100x faster and with 98% fewer errors.

Financial Automation Data Sheet

Download our data sheet to learn how you can run your processes up to 100x faster and with 98% fewer errors.

Financial Automation Data Sheet

Download our data sheet to learn how you can run your processes up to 100x faster and with 98% fewer errors.

Rebate Management Data Sheet

Download our data sheet to learn how you can manage complex vendor and customer rebates and commission reporting at scale.

Top 10 Automation Challenges for CFOs

Learn how you can avoid and overcome the biggest challenges facing CFOs who want to automate.